Ready to get started?

Let’s boost your lead gen.

One of the biggest myths that potential homebuyers suffer under is that they need a 20% down payment to buy a home. It’s crazy in light of the fact that agents do an amazing job of trying to dispel the myth.

The second biggest real estate myth is that consumers with poor credit can’t buy a home. In fact, “bad credit home loans,” “bad credit mortgages” and “how to buy a home with bad credit” are up-trending search terms on Google, especially in California, Texas and Florida.

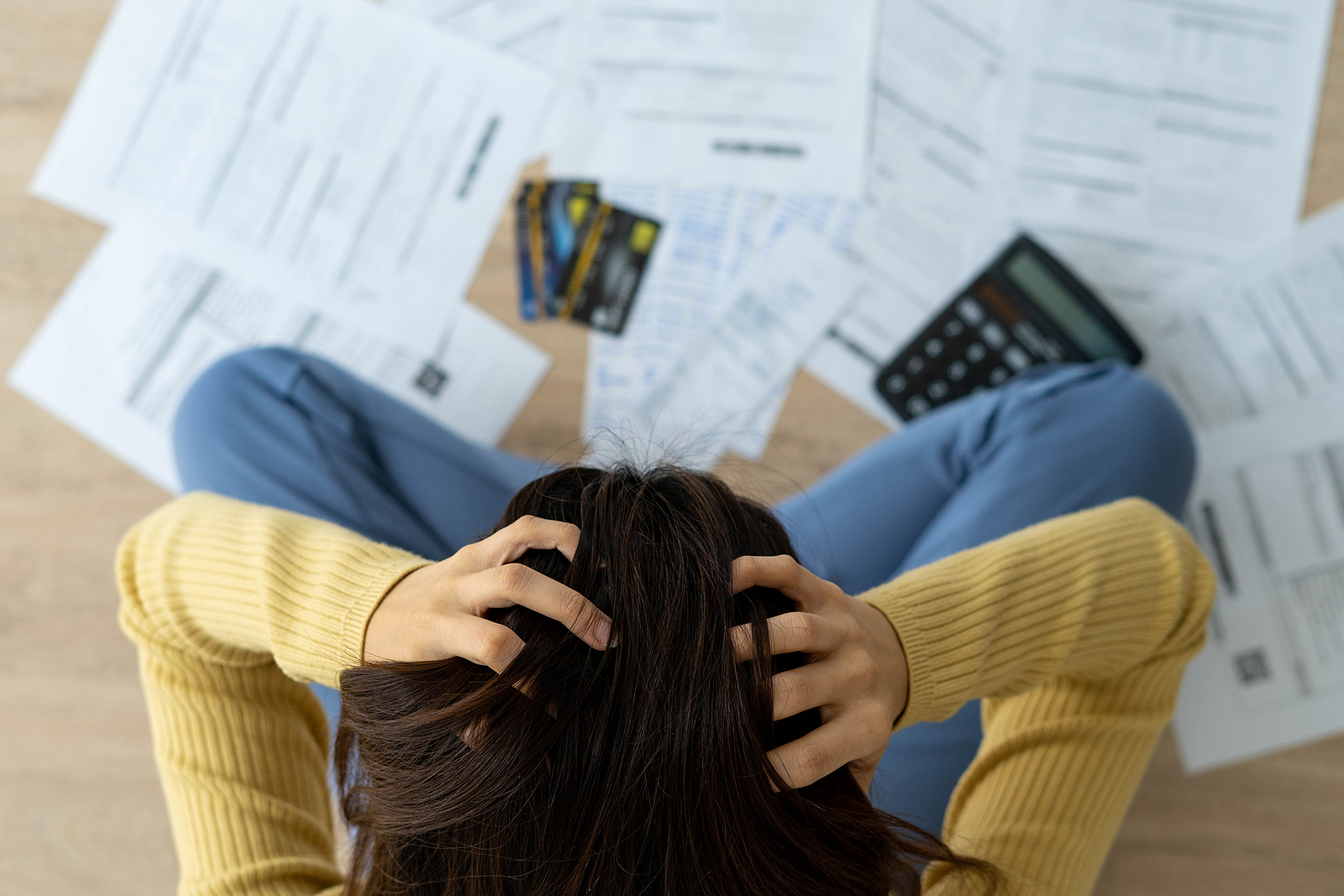

If you have clients who are feeling shut out of the housing market because of a lousy credit score, and you need to close some deals, we have a plan for you: Help them fix their credit scores.

We know what you’re thinking, that credit repair isn’t an agent’s duty. And, it’s not. But lenders apparently don’t feel it’s part of their job description either.

One of our agent friends started his real estate business by generating tenant leads. Many renters want desperately to be homeowners but feel that their bad credit is stopping them. He began counseling them on how to fix their credit scores and eventually worked with most of them on the purchase of their first home.

What’s a “bad” credit score nowadays?

This is something agents need to know and to keep current on. When a lead says that they can’t buy a home because of a lousy credit score, most agents thank them for their time and move on to the next lead.

“What’s your score?” is a far better response. Now, knowing the current average credit score of Americans and the acceptable lowest-score for lenders, you can walk this potential homeowner through the process of cleaning up his or her credit act.

By the way, the average U.S. FICO® Score is 716, according to Ethan Dornhelm at FICO.com.

Although credit scores have risen on a year-to-year basis, even through the pandemic, don’t be surprised if the score falls in 2022 as inflation persists, the mortgage forbearance periods end and folks generally struggle to keep up financially.

To refresh your memory, FICO scores range from 300 to 850. Here’s their score chart:

Although FHA loans are granted to some borrowers with a score as low as 500, they will need to come up with a 10% down payment. With a credit score of 580 there is a 3.5% down payment required.

Since the FHA doesn’t lend money, but guarantees repayment, it’s the lender who has the final say and many of them “… require a score of 620 to 640 to qualify,” according to Tim Lucas at mymortgageinsider.com.

The only way to know for certain where someone stands on the credit front is to order credit reports from Equifax, Trans-Union and Experian.

The free reports are available from the only agency authorized by the federal government, AnnualCreditReport.com. Reports can be ordered online or by phone, at 877-322-8228.

Then, counsel your real estate client to pore over each report, line by line, looking for errors. Is his or her name and other personal information correct?

There’s a long list of common errors in credit reports so direct your client to read about them online at The US Consumer Financial Protection Bureau’s website, consumerfinance.gov.

“About 25% of Americans have an error on their credit reports,” claims Elizabeth Gravier at cnbc.com. If errors are found, they should be reported and/or disputed to the credit reporting agency. Each credit report contains information on how to do this.

Past-due accounts on credit reports account for the largest percentage of a credit score. Thirty five percent of the score is based on payment history.

“This shows whether you make payments on time, how often you miss payments, how many days past the due date you pay your bills, and how recently payments have been missed,” according to the credit management pros at wellsfargo.com.

Payments that are late for 30-days or longer harm scores the most. Let your homebuying clients know this and urge them to raise the proportion of on-time payments by paying on time every month.

Start with any late debt payments that can be brought current quickly.

If your potential client only has one or two late payments on the credit reports, suggest that he or she write a “goodwill letter,” also known as a “goodwill deletion” request.

“While it’s not guaranteed to work, writing a goodwill letter to your creditors could result in negative marks being removed from your credit reports,” according to Emily Starbuck Gerson at creditkarma.com.

Notice that this letter is written to the collection agency or creditor, not the credit reporting agencies.

The chances of this technique working (resulting in a removal of the late pay information) are better if the reason for the late pays was unavoidable, such as “… a personal emergency or a technical error,” Gerson says.

Even that may not sway the creditor. “It never hurts to ask, but in most instances, a goodwill letter won’t result in removal of the negative information,” according to Rod Griffin at Experian.

It’s worth a try though. Get more information on how to write the letter at creditkarma.com.

Thirty percent of a credit score is based on the total amount outstanding on credit cards and loans. Also taken into account:

“High balances and maxed-out credit cards will lower your credit score, but smaller balances can raise it – if you pay on time,” claim the folks at wellsfargo.com.

One of the best ways to quickly raise a credit score is to tackle credit card balances and then use the cards less often, paying the bills as they come in.

Credit history makes up 15% of your client’s credit score. This is why it’s important to keep accounts open even if they’re paid off.

Those with no history or a short one will need to establish themselves. This is typically accomplished by opening credit accounts and paying the bills as they come due.

Secured credit cards are one of the easiest ways to go, according to the experts at Experian.com.

“It will take about six months of credit activity to establish enough history for a FICO credit score,” according to Sienna Wrenn at thebalance.com. She goes on to say that to build up to an excellent score may take years.

Ten percent of the rest of a credit score is based on credit mix. Having different types of accounts, such as credit cards, retail cards and installment loans, “… may help improve your score,” say the loan pros at Wells Fargo.

The final 10% is based on recent credit activity. A lot of activity, such as numerous applications for credit, may bring the score down.

Credit counseling has become quite the scammer-filled industry. Finding a professional isn’t easy, but it’s imperative.

Suggesting a specific counseling service isn’t wise as it opens you to liability. If a client can benefit from credit counselling, urge him or her to visit this page from the Federal Trade Commission, online.

Let’s boost your lead gen.